Online shopping is growing at a faster rate than in-store, but approval rates, fraud rates and the checkout experience haven’t kept pace. Visa is helping close the gap and future-proof the system through richer data sharing, with the Digital Commerce Authentication Program (DCAP), accelerating adoption across the ecosystem.

E-commerce Approval Rates 6.5% lower approval rates for e-commerce vs. in-person transactions1

E-commerce Fraud Rates 6x higher fraud rates in e-commerce vs. in-person transactions2

Improved authorization rates 280bps increase in authorization rates with enhanced data3

Additional performance lift 50bps incremental authorization lift when DCAP standards are met4

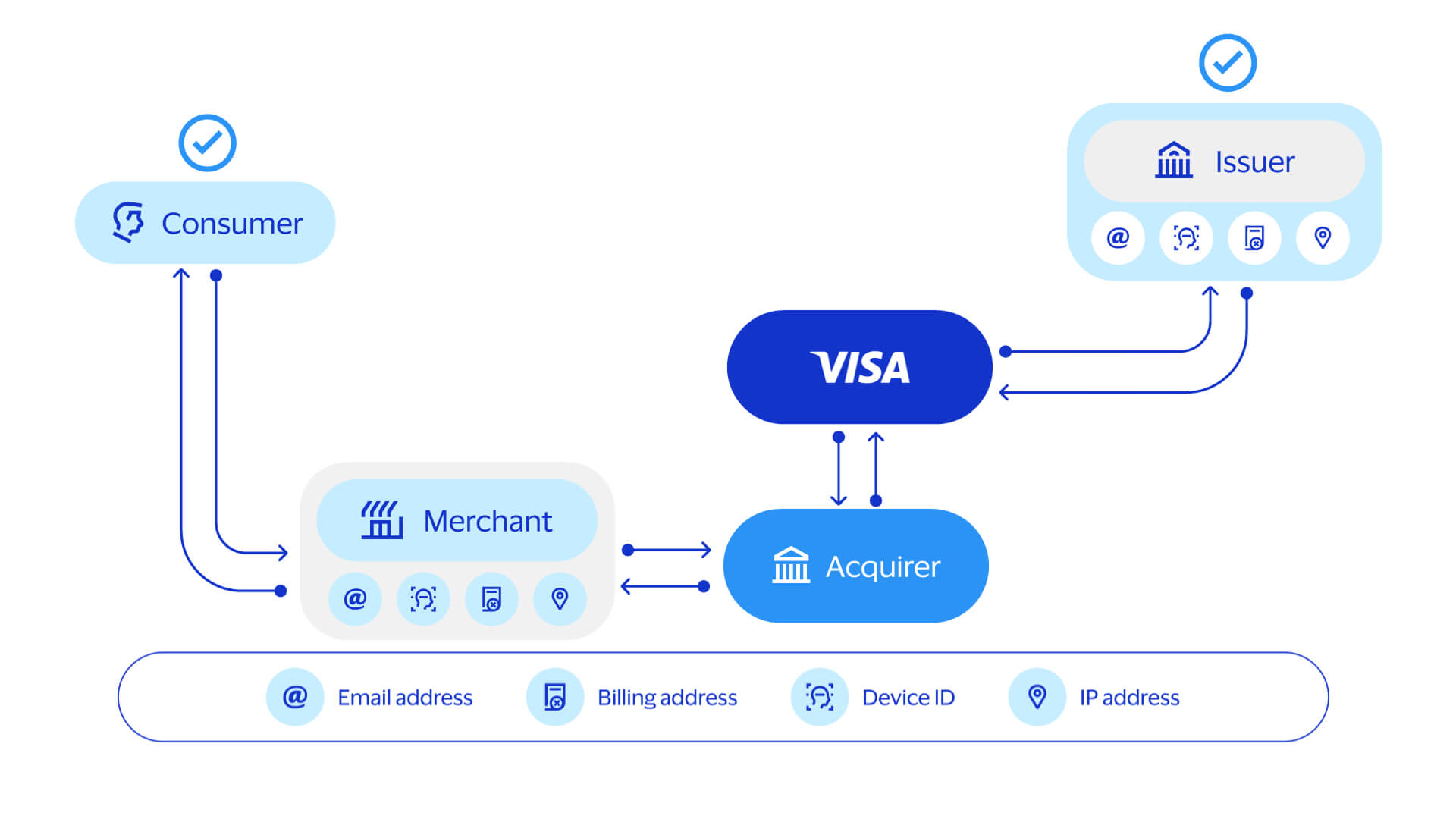

The Digital Commerce Authentication Program is Visa’s initiative to help improve e-commerce authorization performance through enhanced data sharing. By providing a clear, standardized framework for how data is collected, validated and shared across the ecosystem, DCAP helps merchants, acquirers, enablers and issuers adopt and exchange enhanced data more consistently—helping unlock stronger authorization performance.

To participate in DCAP, merchants send four required enhanced data fields—Device ID, IP Address, Email Address and full Billing Address—through one of Visa’s Intelligent Data Exchange solutions. Visa validates and securely delivers this data and risk scores to issuers during authorization, helping support more informed authorization decisions.

Visa Intelligent Data Exchange (IDX) provides the technical pathways for participating in DCAP—connecting merchants, acquirers, enablers and issuers through secure, standardized enhanced data exchange solutions. Three integration paths are available depending on how a participant connects to the Visa network.

| Benefits of Visa | Visa IDX via Visa Data Only | Visa IDX via VTS | Visa IDX API |

| Improved Risk Scores |  | | |

| Token Transaction Support | | | |

| PAN Transaction Support | | | |

| Network Agnostic | |

Our partners are seeing measurable improvements in authorization rates and fraud outcomes through enhanced data sharing. These results translate into more approved transactions and fewer disrupted customer experiences. Explore how leading platforms are putting this into practice.

Square partnered with Visa to share enhanced data with issuers, helping Square achieve approval rates 200 basis points higher than other card-not-present (CNP) transactions while reducing fraud by 29% compared to standard CNP activity.5

See how Adyen and Visa enabled richer enhanced data for an enterprise travel merchant, delivering a 190 bps increase for U.S. authorization rates, while keeping the checkout experience seamless.6

Work with your Visa Account Executive or acquirer partner to explore how enhanced data sharing can increase authorization rates and reduce fraud for your business.

Sources

1VisaNet Data, Global Business Operations, 4Q’CY24, domestic and XB transactions, approval rates are deduped.

2Risk Analytics (MIS), Global Risk Datamart, domestic and XB, including OPCERTS and collections, 12 months ending 3Q CY24, CNP.

3Based on U.S. Card‑Not‑Present transactions, comparing deduplicated authorization rates for Enhanced Data transactions vs non‑authenticated ecommerce (ECI 07), across active merchants, Oct 2025 to Mar 2026.

4Based on U.S. Card‑Not‑Present transactions, comparing deduplicated authorization rates for DCAP‑qualified transactions vs overall Enhanced Data transactions, across active merchants, March 2026.

5Visa and Square, 2025, Real-time data collaboration driving better ecommerce case study.

6Enterprise travel merchant specific case study numbers are from 10/8/25-1/22/26 for the subset of optimized U.S. issuers only. U.S authorization rates. Methodology note: Focused on a subset of optimized issuers. Results are based on an Adyen‑run pilot comparing transactions with Enhanced Data enabled (“Yes”) versus a control group (“No”). Analysis focuses on first‑attempt approval rates (first approved / initiated). Transactions included domestic and cross border, consumer‑initiated eCommerce purchases processed via Adyen. Wallets, standard 3D Secure flows, merchant‑initiated transactions, and account funding transactions were excluded.